Few Signs of Trouble on the Industrial Front

The sector continues to stand strong despite rising inflation and interest rates.

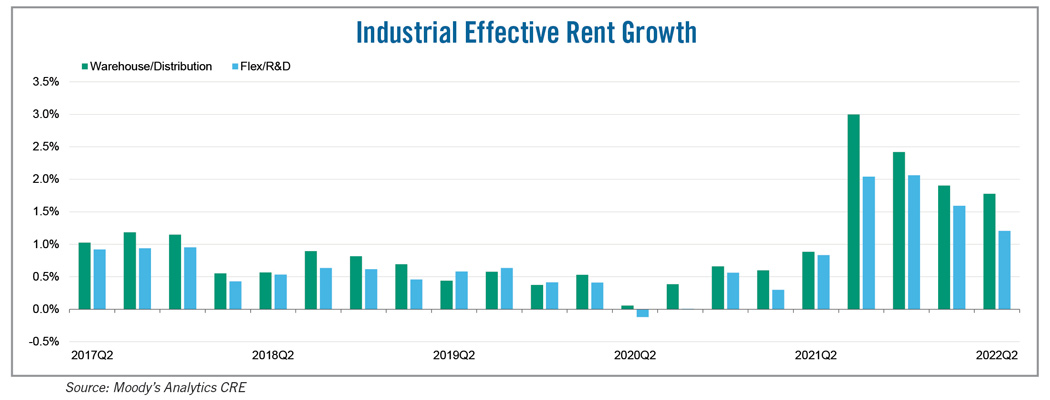

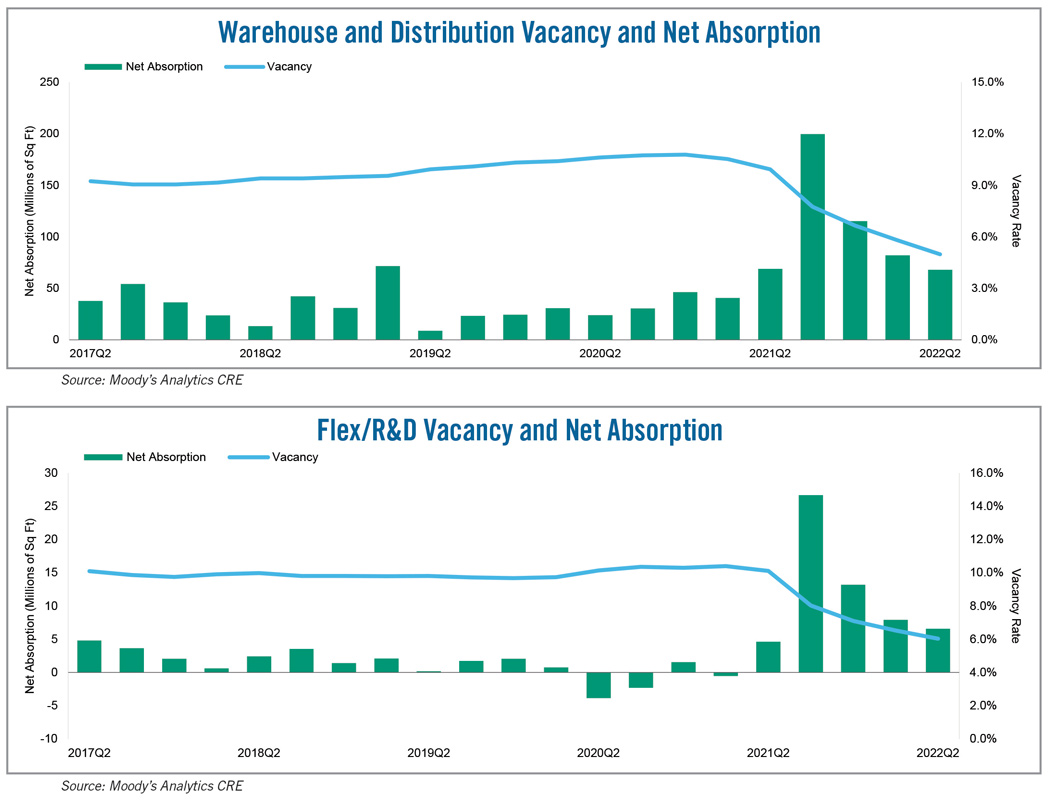

Among commercial real estate sectors, industrial emerged as the clear winner following the pandemic-induced recession. And despite signs of headwinds on the horizon, both warehouse/distribution and flex/R&D continue to exhibit stellar performance.

The sector is likely to stay buoyant into 2023 as the outlook remains positive for the underlying demand drivers, notably the increase in spec construction of properties. This is particularly true for cold storage facilities, which are considered safe investments because they store essential consumer staples such as food and medicine and are thus generally insulated from external macroeconomic shocks.

However, concern over the current macroeconomic environment and what the short-term future might hold raises the question of how the industrial sector will fare going forward. Inflation, already quite high at the start of 2021, has risen sharply since the second half of 2021. By June 2022, the figure came in at 9.1%, a four-decade high, though by late summer there were signs that inflation might be slowing.

As part of the Federal Reserve’s dual mandate to keep prices stable and ensure full employment, raising interest rates is one of the main monetary policy tools it has to control inflation. This increases the cost of borrowing, which can have significant effects on the industrial sector.

The obvious effect is that construction gets more expensive because of the higher cost of borrowing as well as rising prices for raw materials resulting from inflation. While the industrial sector currently has a healthy pipeline of projects planned as well as under construction, given the record-setting demand observed in the second half of 2021, combined with ongoing elevated demand through 2022 (both observed and forecast), room still exists for both rent and occupancy growth.

E-Commerce Drives Demand

E-commerce as a percentage of total retail sales is an important metric for the industrial sector, as it requires a larger amount of square footage than traditional retail due to inventory, packaging and shipping requirements.

Online sales increased more than 30% from the first quarter of 2020 to the second quarter of 2020 as consumers relied on e-commerce amid pandemic-related closures and stay-at-home orders. Online now represents 14.3% of total retail sales as of the first quarter of 2022. This number is lower than its historical peak of 16.4% in the second quarter of 2020, but still a notable gain from the first quarter of 2020 when it stood at 11.9%, the highest figure until that point. This indicates that e-commerce growth is returning to its original trajectory. Nonetheless, the substitution of e-commerce for bricks-and-mortar is likely to continue its growth through the next few years, with the potential to reach 20% of total retail sales within a decade.

Consumer Spending Concerns

Future demand for warehouse/distribution properties is largely driven by consumer spending, whether via e-commerce or through bricks-and-mortar retail. Retail sales have generally risen since the second quarter of 2020. Sales across all sectors have been strong for the past few months, indicating that consumers are willing to spend.

Sales in the first half of 2022 continued the robust trajectory seen since the pandemic-fueled structural break in April 2020. However, high inflation has contributed in part to sustained increases in spending as consumers are now paying substantially more for the same basket of goods.

Consumer sentiment, on a sharp decline since mid-2021 amid inflation worries, continues to fall on the increasing likelihood of a recession. It reached a low of 58.4 in May, a level not seen since October 2008 during the height of the Global Financial Crisis. The fact that consumer sentiment is now lower than it was in April 2020 indicates that rising prices are eclipsing any pandemic concerns. It also points to a possible significant slowdown in spending on the horizon, which could be consequential for the warehouse/distribution subsector.

Factoring in expectations that have revised real GDP growth downward to less than 2% in both 2022 and 2023, as well as rising interest rates that are boosting the cost of borrowing, retail sales are likely to face downward pressure in the second half of this year. Any substantial declines in consumer spending that might result from inflation and rising interest rates will dampen demand for distribution/warehousing properties.

The good news is that warehouse completions prior to 2020 were modest, and global supply chain issues in recent months slowed the pace of construction. Because of this, the sector is not currently oversaturated in a way that would have drastic negative impacts on key metrics such as rents and vacancies if there is a shock to demand-side movements.

Ermengarde Jabir, Ph.D., is an economist with Moody’s Analytics.

RELATED ARTICLES YOU MAY LIKE

From the Editor: As the Economy Improves, What’s Next for CRE?

Fall 2023 Issue

Construction Cost Challenges Shift from Materials to Labor

Fall 2023 Issue