Commercial Real Estate's Economic Environment Has Been Nearly Perfect

Inflation and unemployment remain low, but how long will these conditions last?

The economic environment for owners of commercial real estate has been extremely favorable for the past few years. The strong economy has produced a healthy leasing environment and allows for reliable increases in rent per square foot.

The U.S. economy is in the midst of its lengthiest expansion cycle in history. Approximately 21 million net new jobs have been created to date since the end of the Great Recession in 2009. Unemployment has hovered around a 50-year low for months. Consumers have been especially active, helping to keep brick-and-mortar retail going even as fulfillment centers tied to the burgeoning e-commerce economy sprout up in metropolitan and rural areas alike.

The Current Situation

But a strong economy represents only one element of this nearly ideal environment. Despite a strong labor market that is delivering its fastest wage growth in roughly a decade, inflation has remained benign. That has helped keep borrowing costs low. A prominent measure of inflation, the Core Personal Consumption Expenditure (PCE) Deflator, indicates that inflation over the past year has been meaningfully below 2%, the Federal Reserve’s stated target.

In response to a weakening global economy, a recently inverted yield curve and concerns regarding the economic impacts of ongoing trade disputes, the Federal Reserve has already cut interest rates three times in 2019 after raising them nine times between December 2015 and December 2018. They now range from 1.75% to 2%. The reduction in rates makes it more likely that investors will continue to look for opportunities to generate investment yield, including through ongoing investment in commercial real estate.

Ironically, the weak global economic environment and the prevalence of negative interest rates in Japan and in much of Europe has induced considerable global capital to flow into the U.S. Last year, global investors infused New York’s commercial real estate market with nearly $17 billion based on a report by Real Capital Analytics. On a per-capita basis, few if any metropolitan areas have experienced as much foreign investment intensity in commercial real estate as the Washington, D.C., metropolitan area. In 2018, foreign investment totaled $83.6 billion per 100,000 residents in the region. New York was close behind with $81.7 billion for every 100,000 residents, followed by the San Francisco Bay Area with $65.4 billion.

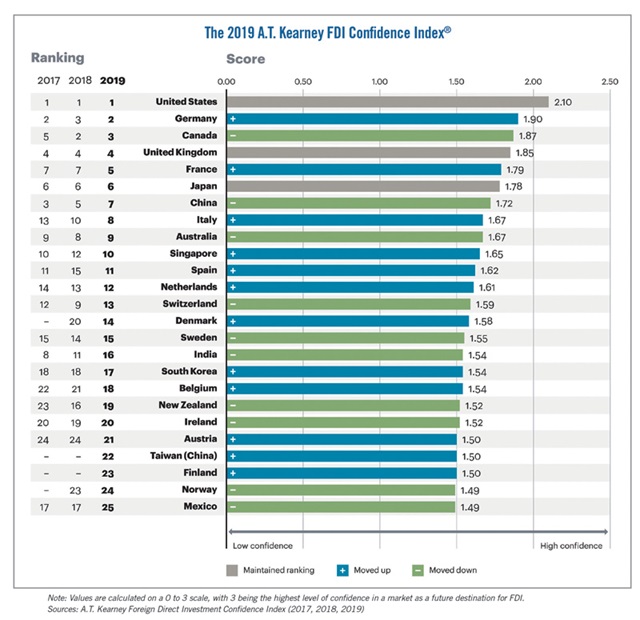

Foreign interest in U.S. assets has been dispersed across asset classes. A.T. Kearney, a global management consulting firm, produces the Foreign Direct Investment (FDI) Confidence Index. Based on a survey of top executives from Global 1000 companies, the U.S. ranks first in the world in terms of generating confidence among foreign investors once political, economic and regulatory factors are taken into account. Germany ranks a distant second, and Canada is third. America has held the top spot for seven years running because of its “sustained and robust economic expansion in recent years,” according to the FDI report.

Foreign investors haven’t been the only actors expanding demand for commercial properties. Real estate investment trusts, insurers, pension funds, private equity firms, hedge funds and others searching for yield in the context of low interest rates around the developed world have also played important roles. Because of that, capitalization rates have been low as buyers appear willing to fork over significant sums in the continuous search for income.

According to CBRE’s “North America Cap Rate Survey H1 2019,” capitalization rates remained modest during the first half of 2019. For industrial properties, cap rates fell 5 basis points to 6.27%.

“Strong market fundamentals — low vacancy, robust e-commerce-driven tenant demand and rent growth — continue to attract investors to industrial assets, increasing values and leading to sustained cap rate compression,” Jack Fraker, CBRE’s global head of industrial and logistics, recently told the McMorrow Reports. “Due to high competition for core properties, investors remain interested in assets with a higher risk profile. Investors are looking beyond year-one cap rates and to the increasing returns provided by predictable rental rate growth throughout the life of the deal.”

Among central business district (CBD) office properties, cap rates fell 4 basis points to 6.67%, while cap rates for suburban properties stood at 7.91%, falling by a basis point.

“Office cap rates should remain stable for both CBD and suburban properties over the next six months, supported by strong tenant demand for space, favorable investment sentiment, and expectations for stable or decreasing interest rates,” says Christopher Ludeman, CBRE’s global president of capital markets, in the company’s “North America Cap Rate Survey H1 2019.”

Looking Ahead

Risks to commercial real estate and the broader economy are growing, threatening today’s ideal environment for commercial markets. Many forecasters predict the onset of a recession in approximately one year’s time. There are many factors at work, including the trade war with China, concerns regarding the vulnerability of elevated asset prices, lingering inflationary fears and a steadily weakening global economy.

But perhaps the greatest risk emerges from next year’s presidential election. The issue is not necessarily the election’s ultimate result, but the fact that one is going to happen. The policy differences between the incumbent and any conceivable challenger are significant. The result will be an elevated level of uncertainty, likely translating into many economic actors postponing major purchases and investments.

Combined with other sources of vulnerability, the election may be enough to put an end to the longest expansion in American history.

Anirban Basu is the chairman and CEO of the Sage Policy Group in Baltimore.

RELATED ARTICLES YOU MAY LIKE