Why Investors Are Flocking to Student Housing

Purpose-built student housing has matured into an institutionally acceptable asset class.

ONCE CONSIDERED a niche subset of the rental housing sector, purpose-built student housing (PBSH) has matured into an institutionally acceptable asset class. A large and increasingly college-bound population of young adults, set against a backdrop of underinvestment in on-campus housing, have together created a housing shortage for college students in many markets. Developers have been seeking to fill this with off-campus student housing.

A Unique Product

The key differentiator between PBSH and traditional apartments is the leasing model. PBSH leases by the bed, not the unit. If a roommate decides to drop out at winter break, the remaining roommate — and his or her parents — are not on the hook for the entire amount of the unit’s rent, only for their respective portion. A typical unit consists of three bedrooms and three bathrooms, as well as a shared kitchen and living-dining area.

Paula Poskon

Another differentiator is the leasing cycle. Generally, leases are based on a 50-week time frame, payable in 12 monthly installments. This allows for the annual “turn” ahead of the start of the academic year, when most tenants move out, giving the owner/operator just two weeks to complete needed repairs and maintenance before new tenants move in. Thus, unlike a traditional apartment that can be rented any time, a PBSH community that starts the school year with an empty bed will likely see it remain empty for the entire coming year. On the flip side, however, is the high visibility of cash flows. With tenants in place by the start of the school year, forward 12-month revenue is essentially locked in.

With steady demand year-over-year and limited comparable competing product, net operating income (NOI) annual growth produced by stabilized assets owned for more than one year (same-store) has remained in a stable range of 1 to 5 percent over the past five years. Thus, while it did not enjoy the double-digit growth seen in the apartment sector during the economic recovery, PBSH was likewise shielded from declining NOI during the downturn.

Bill Bayless, CEO of publicly traded American Campus Communities (ACC), often cites in his investor presentations the fact that ACC has produced 11 consecutive years of positive same-store NOI growth, even through the Great Recession. That track record dates back to the company’s initial public offering in 2004, a stellar track record by any measure.

Institutional Investment Increases

This predictability of cash flows and recession resilience is attracting increasing institutional investment into PBSH, particularly at a time when other real estate sectors may be viewed as being closer to the end of the cycle. For example, the two largest transactions last year each exceeded $1 billion, and neither of the two public REITs involved in PBSH were among the buyers.

Chicago-based private equity firm Harrison Street Real Estate Capital LLC acquired the assets of Campus Crest Communities, which had been one of only three publicly traded REITs specializing in PBSH, in a roughly $2 billion deal. Similarly, Scion Group, also based in Chicago, formed a joint venture with equity partners Canada Pension Plan Investment Board and GIC Real Estate to acquire a portfolio of approximately 11,000 beds serving 18 campuses from University House Communities Group in a deal valued at about $1.4 billion. Despite its size, this joint venture has remaining capacity to continue making acquisitions.

Commenting on the influx of capital into PBSH, Dorothy Jackman, managing director at Colliers International and a broker specializing in student housing transactions, notes that cross-border dollars account for 40 percent of total sales year to date, up from just 2 percent in 2013.

Yet, these two transactions are the exception in PBSH, not the norm. Justin Glasgow, who specializes in student housing at Cushman & Wakefield, says PBSH has “only a few well-capitalized, fully integrated owner/operators and a small number of PBSH-focused equity capital sources. The result is a relatively small sector with just a handful of large investors funding multiple competitors. We see a significant shift among investors interested in the space, both traditional and nontraditional, to partner on an exclusive or near exclusive basis to get involved.”

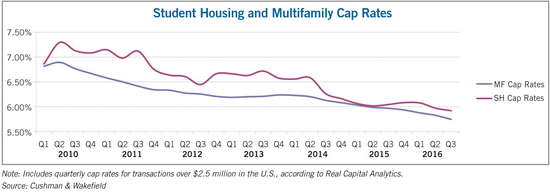

Not surprisingly, the impact of increased institutional investment has been compressing cap rates, in particular closing what had been a historical spread of 50 to 75 basis points above traditional multifamily housing.

This has compelled the largest players to begin recycling capital in larger volumes. In late 2016, ACC sold a portfolio of roughly 12,000 beds in a transaction exceeding $500 million, at a reported 6.1 percent average going in economic cap rate, calculated using NOI adjusted for recurring capital expense and management fees. Proceeds, along with those of asset sales earlier in the year, are being redeployed into the company’s development pipeline, currently projected to deliver $600 million worth of assets by the start of the 2017/2018 academic year and another approximately $230 million already underway for 2018/2019. With development yields still offering an approximately 150 bps spread to acquisition cap rates, it is logical to see the dominant players weighting capital allocation more heavily toward development.

The more relevant question for these players, rather than acquisition versus development, becomes where to focus development investments. For the two publicly traded REITs, ACC and Education Realty Trust (EDR), that answer brings the story full circle.

A New Model

The emerging trend in PBSH, led by these two companies, is the public-private partnership model. REITs are partnering with universities to replace aging on-campus student housing and add new housing capacity on campus. In the last five years, such investment by the two companies has grown from zero to $2 billion. Their respective operational track records, financial transparency and access to the spectrum of options in the capital markets position them as a duopoly to capture this growing opportunity set.

The university gets new housing, helping it attract the best students and win the matriculation battle, without drawing on its own balance sheet. The companies add assets to their portfolios — assets that have even lower leasing risk and thus more stable cash flows than their off-campus student housing assets.

Key terms of such partnerships typically include a long-term ground lease exceeding 50 years, often with multiple 10-year renewal options; noncompete provisions; collaborative marketing efforts; and ground lease payments by the developer that are adjusted based on how much non-revenue generating space the university wants in the structure, such as classrooms or faculty offices.

With the public REITs weighting capital allocation more heavily to on-campus development, some smaller private players see a window of opportunity to ramp up acquisition volume. In their view, the REITs are moving to a quasi-infrastructure business model and effectively ceding their leadership as industry consolidators. “That’s just nonsense,” says Randy Churchey, CEO of EDR. “Looking back over the last decade, two-thirds of the REITs’ growth has come from acquisitions, and I suspect when we look back 10 years from now, the same will still be true.”

Paula Poskon, founder, STOV Advisory Services

RELATED ARTICLES YOU MAY LIKE