Demography is Destiny for Commercial Real Estate

Population shifts could portend big changes for the industry.

Second in a two-part series.

While it is often said that the performance of an individual property is a function of three factors (location, location, location), one could make the argument that the performance of the overall commercial real estate segment is a function of its own triad of elements: demographics, demographics, demographics. Indeed, over the course of time, there is a strong correlation between demographic trends during a given decade and the performance of commercial real estate during that decade and the next.

Take the 1980s as an example. During that decade, Americans migrated toward cities in massive numbers. The New York metropolitan area remained America’s largest, of course, but that’s not where the population growth was concentrated. Regional population growth in New York that decade was in the range of 3%.

It was in the Sun Belt where population really took off. The Orlando metropolitan area expanded its population by more than 50%. Other movers and shakers included Phoenix and San Diego, where population expanded 41% and 34%, respectively.

But the primary point is that metropolitan areas throughout the nation continued to expand as farming productivity surged and as fewer people were needed to operate rural economies. An analysis by the USDA’s Economic Research Service found that between 1948 and 2011, the U.S. population more than doubled as did agricultural output, even though the segment used about 25% less farmland and 78% less labor.

Meanwhile, the emergence of professional and financial services created new opportunities for highly educated workers, with virtually all those opportunities located in cities and upscale suburbs. Many young professionals headed to cities to become lawyers, doctors or stockbrokers. All of this was good for commercial real estate, which surged in value for much of the 1980s.

Of course, other factors were at work, including the pre-1986 tax code, declining inflation and interest rates, and the acceleration of globalization. In 1981, President Ronald Reagan signed the Economic Recovery Tax Act of 1981 into law. That legislation included several provisions that improved rates of return on certain types of properties, including by accelerating depreciation of commercial real estate.

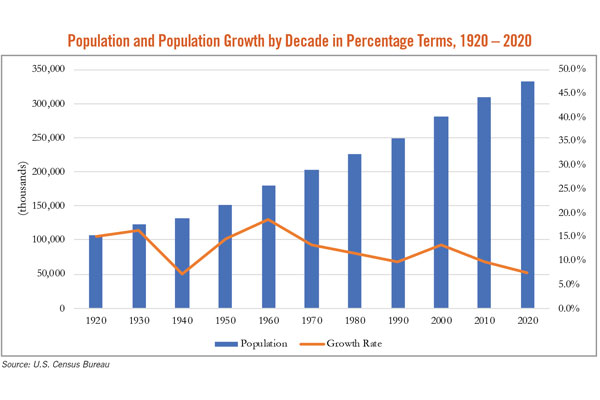

Nonetheless, demographics were critical in leveraging these other factors. A February 1991 New York Times article indicated that for the first time in U.S. history, most of the country lived in metropolitan areas of more than one million people. No wonder the ‘80s and ‘90s were associated with the construction of so many residential and commercial high-rises.

There was another major factor at work — immigration. An analysis of data from the Census Bureau’s decennial census and population estimates program found that between 1980 and 1990, more than one-fourth of America’s growth was attributable to immigration. Many of those immigrants ended up in cities. From 1980 to 1984, metropolitan areas grew only about one and a half times as fast as nonmetropolitan areas. But from 1984 to 1988, metropolitan areas expanded population nearly four times as fast as nonmetropolitan areas.

Times Have Changed

That was then; this is now. America’s population growth has slowed in recent years. (See “Preliminary Census Findings and Their Implications for Commercial Real Estate” from the Fall 2021 issue of Development magazine.) That was certainly true of 2021. The Census Bureau’s Vintage 2021 Population Estimates indicate that the nation’s population expanded only 0.1% last year. Census Bureau data also indicate that 2021 is the first time since 1937 that America’s population expanded by less than one million people.

As indicated by the bureau, slower population growth has become a feature in the U.S. for several years, the result of declining fertility, slower net international migration, and increased mortality due to an aging population and more recently COVID-19. Since the mid-2010s, births and net international migration have been in decline while deaths have been on the rise. In many instances, population is in decline.

Nowhere did population fall faster in 2021 than in the District of Columbia, which recorded a 2.9% decline in population. Other geographies associated with declining population are New York, Illinois, California and Massachusetts, states that are collectively home to many of America’s largest cities. Meanwhile, the list of states with the fastest population growth in 2021 includes Idaho, Utah, Montana and South Dakota.

If demographics are destiny, these trends do not portend favorably for commercial real estate, at least in large, older American cities. The confluence of the pandemic and the technological response to it will place further pressure on commercial real estate occupancy and valuation.

According to an economic report published by Glassdoor.com, the share of job searches that included remote opportunities grew 360% between June 2020 and June 2021. According to the Bureau of Labor Statistics, approximately 42 million American workers have the ability to work remotely. Thus, while U.S. gross domestic product surged past its pre-pandemic level by 2021’s second quarter, U.S. office vacancy continued to rise during 2021’s latter half.

Business meetings conducted via Zoom, Microsoft Teams or other platforms create additional issues for commercial real estate, as does the growing pervasiveness of online shopping. While growth in certain communities like St. Petersburg, Florida, or Austin, Texas, can more than countervail these centrifugal forces on cities, many other communities will find increasingly barren central business districts, delinquent shopping centers, marginal hotels and semi-abandoned office buildings.

As always, there are actions that real estate operators can take. A survey conducted by Clever Real Estate in December 2020 asked respondents what office-building amenities were most appealing to them. At the top of the list was close proximity to coffee shops and lunch options, with nearly half (49%) of respondents including those in their response. Close parking (45%) and on-site food options (44%) were also near the top of the list.

In the final analysis, the economics of commercial real estate will remain challenging in 2022. In addition to behavioral changes that have altered (and often reduced) spatial requirements, the year will likely be associated with lingering labor market tightness and rising interest rates. Of course, it is conceivable that by year’s end, we could be talking about yet another resurgence of the pandemic.

Anirban Basu is the chair and CEO of the Sage Policy Group in Baltimore.

RELATED ARTICLES YOU MAY LIKE

Construction Cost Challenges Shift from Materials to Labor

Fall 2023 Issue