Industrial Space Demand Forecast, Third Quarter 2019

Release Date: August 2019

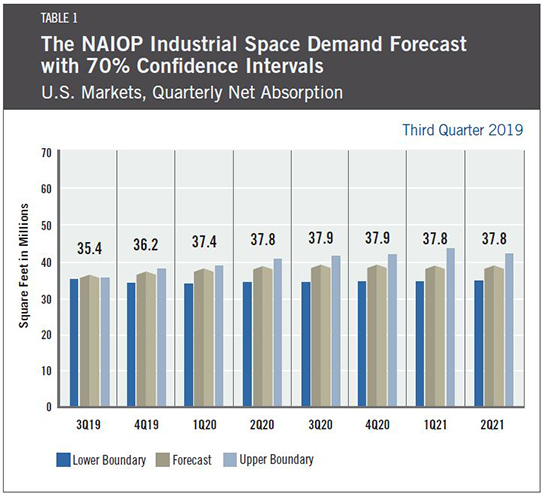

Industrial Demand Forecast Decreases as Economy Slows

The forecast for net industrial space demand has decreased amid slower growth in the U.S. economy. Absorption is now expected to average 37 million square feet per quarter for the next two years, according to Dr. Hany Guirguis of Manhattan College and Dr. Joshua Harris of New York University. This is a significant slowdown from the average 60 million square feet of quarterly net absorption experienced during 2017 and 2018.

There are two reasons for the forecasted slowdown. First, GDP growth in 2019 is now expected to be in the range of 1.75 percent to 2.25 percent, down from prior expectations of 2.5 percent to 3.0 percent. A slowdown in business investment is likely to be a primary driver of lower GDP growth rates, and it will also affect industrial real estate expansion. Second, net completions of industrial space are growing at a slower pace. The average quarterly completions fell to 42 million square feet in the first half of 2019, down from an average of 54 million square feet per quarter during 2017 and 2018. Supply and demand are likely to stay in balance for the industrial sector; therefore, rents and vacancy rates should remain stable in many markets nationwide.

During the first half of 2019, the economy experienced several unique shocks. These included the prolonged government shutdown, increased tariffs and trade tensions (particularly with China and Mexico), and a multitude of global events such as the slowdown in Chinese economic growth and continued Brexit uncertainty. The Conference Board’s Measure of CEO Confidence stayed in negative territory during the first and second quarter — a major reversal from the positive sentiment of the past several years. These factors also contributed to the underperformance of the industrial markets so far this year; although 117 million square feet was previously forecast, only 67 million square feet were actually absorbed.

On a positive note, the Federal Reserve recently announced a quarter-point cut in interest rates in response to the reversal in economic sentiment. A recession is not likely in the near-term, but a general slowdown appears already underway; the first report of GDP growth in the second quarter fell to 2.1 percent from the 3.1 percent annualized result of the first quarter.

Despite the reduced forecast, there are chances for upside surprises in industrial activity during the near-term. First, a positive resolution to ongoing trade talks may give industrial enterprises more confidence in the latter half of 2019. That could bring back some of the expansion plans delayed in the first half of the year. Second, the Federal Reserve rate cut, coupled with the low unemployment rate and strong growth in retail sales, could be a catalyst that restores positive business sentiment. Lastly, as Amazon pushes to expand one-day delivery, there could be an increase in last-mile distribution center leasing. This could lead to better national results, but it will reflect a structural shift in the industrial market and not a reversal of current trends.

Key Inputs and Disclaimers

The predictive model is funded by the NAIOP Research Foundation and was developed by Guirguis and Dr. Randy Anderson, formerly of the University of Central Florida. The model, which forecasts demand for industrial space at the national level, utilizes variables that comprise the entire supply chain and lead the demand for space, resulting in a model that is able to capture the majority of changes in demand.

While leading economic indicators have been able to forecast recessions and expansions, the indices used in this study are constructed to forecast industrial real estate demand expansions, peaks, declines and troughs. The Industrial Space Demand model was developed using the Kalman filter approach, where the regression parameters are allowed to vary with time and thus are more appropriate for an unstable industrial real estate market.

The forecast is based on a process that involves testing more than 40 economic and real estate variables that theoretically relate to demand for industrial space, including varying measures of employment, GDP, exports and imports, and air, rail and shipping data. Leading indicators that factor heavily into the model include the Federal Reserve Board’s Index of Manufacturing Output (IMO), the Purchasing Managers Index (PMI) from the Institute of Supply Management (ISM) and net absorption data from CBRE Econometric Advisors.

ISM, the Federal Reserve and CBRE Econometric Advisors assume no responsibility for the Forecast. The absorption forecast tracks with CBRE data and may vary when compared with other data sets. Data includes warehouse, distribution, manufacturing, R&D and special purpose facilities with rentable building areas of 10,000 square feet or more.

Actual Versus Forecast

Although it got off to a slow start during the first half of 2018, the industrial market ended 2018 by performing closely with the previous forecast of net absorption. In 2018, 229.5 million square feet of industrial space was absorbed, inline with the forecast of 222.2 million square feet.

Initial and Ongoing Research

In 2009, the NAIOP Research Foundation awarded a research grant to Anderson and Guirguis to develop a model for forecasting net absorption of industrial space in the United States. That model led to successful forecasting two quarters out. A white paper describing the research and testing behind the model for NAIOP’s Industrial Space Demand Forecast is available.

The model was revised in 2012 to forecast eight quarters out. For this longer term forecast, Guirguis and Harris utilize the average central tendency forecast of the unemployment rate and growth rate of real GDP, provided by the seven members of the Board of Governors and the 12 presidents of the Federal Reserve Banks during the most recent Federal Open Market Committee meeting. Their forecasts are the independent variables in the equations. The forecasts usually vary from one year to another, so different techniques are applied to convert the yearly forecast to a quarterly one, in order to create the quarterly forecasts for net absorption. The estimated coefficients on the independent variables are estimated with the time-varying Kalman filter.