Real Estate Crowdfunding: Solid Growth, But Challenges Remain

Among them: Unrealistic expectations and the possibility of an economic downturn.

The real estate crowdfunding industry has been growing steadily for years, and with each turn of the calendar it becomes more firmly established as an attractive option to traditional property syndications or mainstream passive investments, such as stocks and bonds.

After years of building solid track records, albeit in a conducive environment of rising real estate values, the only challenge to the real estate crowdfunding industry is itself — how does the industry continue to maintain growth at the explosive pace seen during the past few years?

The Backstory

According to the author’s analysis of data from the Securities and Exchange Commission, crowdfunding industrywide produced 25% of all capital raised for real estate private equity in 2020 despite being “born” — actually, merely conceived — only 10 years ago.

The largely unheralded inception of the real estate crowdfunding industry was in the Jumpstart Our Business Startups or “JOBS” Act, passed by Congress in 2012. This modified or expanded certain restrictive aspects of the 1933 Securities Act.

In a nutshell, the key feature of the JOBS Act was that it allowed for general solicitation — including, in the modern age, the online solicitation — of investors for private-equity offerings.

Before 2012, the traditional real estate syndications industry, which is part of the private-equity-raising trade, had been something of a small club. It was often uncompetitive and lacked transparency. Real estate syndication offering memorandums were paper documents, and investors had difficulty comparing one syndicator’s offerings against industry averages, or even finding past track records. The opaque nature of the industry led to predictable shortcomings.

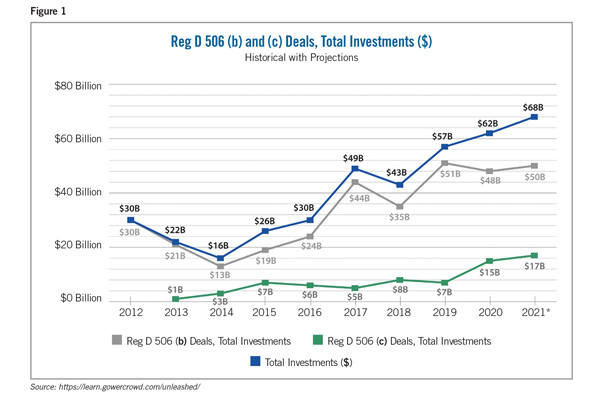

Thanks to the internet, most real estate crowdfunding offering memorandums are online. As can be seen in Figure 1, the majority of real estate crowdfunding deals are Reg D 506 (b) transactions (the middle, lighter gray line). These allow for solicitation of only investors with whom the sponsor has a pre-existing relationship. This is the pre-JOBS Act, pre-crowdfunding formula for raising capital, where sponsors were required by regulations to conduct one-on-one, in-person meetings with investors.

The new Regulation 506 (c) (the lower, slightly darker line) shows the growth trend since the passage of the JOBS Act (the inception of crowdfunding) and the subsequent ability for sponsors to market themselves and their deals openly, online, with no requirement for a pre-existing relationship with a prospect.

By forcing everyone to work remotely and avoid in-person meetings, the pandemic has accelerated the trend for capital formation to be conducted online. As shown in Figure 1, crowdfunded syndications more than doubled in dollar volume from $7 billion in 2019 (pre-pandemic) to $15 billion in 2020. Notable also is that during this same period, 2019-2020, traditional capital formation (the non-crowdfunded method) actually declined from $51 billion to $48 billion.

The crowdfunding model for commercial real estate capital formation appears to be catching up with traditional means of raising capital. Sponsors and individual investors are now allowed to meet remotely online, establish a relationship without the need for direct, personal interaction, and engage in commerce together.

Outlook

In general, the outlook for the real estate crowdfunding industry is bright, and even the rising specter of inflation in 2022 could be as much a boon as a pitfall. As inflation rises, investors seek ever-increasing yields, and hard assets like real estate offer compelling options that are now available for the first time to everyone thanks to the growth of crowdfunding.

Crowdfunding has revealed the inner workings of real estate investing to the public, making it less opaque and easier for individuals to understand, assimilate and invest. As real estate investment opportunities become even more widely visible online, demand should continue to rise as investors seek not only alternatives to stocks and bonds, but also a hedge against inflation.

Apart from the rapid growth of the industry during the pandemic, leading crowdfunding platforms like CrowdStreet are seeing increasing interest in crowdfunding by institutional investors and sponsors nationwide. For example, they have seen individual crowdfunded equity capital raises exceed $40 million — a hitherto unimaginable scale for what many continue to erroneously think is a donation- or startup-based way to raise capital.

The Challenges

Nevertheless, the challenge to the real estate syndication industry is real, and there are legitimate concerns about what will happen to the image of crowdfunding when there is a sustained decline in general real estate values during the next economic downturn.

Many crowdfunded transactions, as seen in offering memorandums, assume a robust rise in the value of the relevant real estate or portfolio en route to an exit strategy, often in connection with a property makeover. When those expectations are not met, a naïve community of first-time real estate investors will learn the hard way that real estate, like all other asset classes, is subject to cyclical ups and downs.

Certainly, optimism is necessary in any business, and without projections few would invest in any enterprise, real estate included. Still, the pattern seen in past real estate downcycles will be repeated: Investors get angry at scant returns or even losses, and then start hiring lawyers and forensic auditors to review profit splits, management fees and sponsor prerogatives.

Naturally, the financial-media headlines will center on the worst-performing deals, as well as those crowdfunded transactions that favored the sponsors most over the passive investors. The cases of simple fraud and busts will also get plenty of coverage, and the crowdfunding industry will have to weather the storm.

Sustained declines in property values are hardly the stuff of legend, even if presently the prospects for a real-estate sector value slump appear remote.

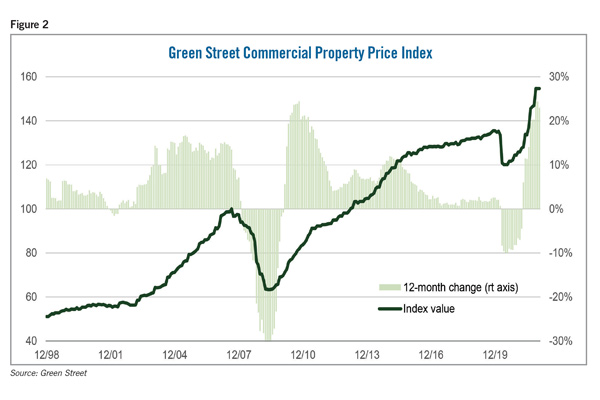

As seen in Figure 2, general commercial real estate values tumbled nearly 40% in the Great Recession of 2007-2009, and they did not nominally recover until nearly 2014. It’s notable that during the decline in values at the onset of the pandemic, crowdfunded transactions more than doubled. That suggests a hunger for the asset class among the investing public despite temporary market upsets.

Yet many present-day crowdfunded real estate syndications assume 20%-plus rises in property value en route to their eventual sale, when investors expect the bulk of their gains to be realized.

If there is a real estate contraction, investors will not reap the projections featured in offering memorandums, and even if the market is at fault, the sponsors — and crowdfunding — will get the blame.

Because of this, the crowdfunding industry may wish to consider measures that encourage conservative or at least multiple scenario-dependent financial projections, and to standardize sponsor literature, fees, payouts and profit splits.

And investors would be wise to disavow themselves of the tendency to expect returns on a quarterly basis that they have become accustomed to with traditional investments such as stocks. They should take the long-term view that prudent real estate veterans know will see them through the bad times to the brighter days that always return.

Adam Gower is the founder of the National Real Estate Forum podcast.

RELATED ARTICLES YOU MAY LIKE