Construction is Recovering but Faces Challenges

Materials costs have been on a rollercoaster ride for the past year.

The long skid in nonresidential construction spending that began with the onset of the pandemic in early 2020 appears to be nearing the bottom, while multifamily construction continues to exceed early expectations. However, the path forward remains bumpy and uncertain.

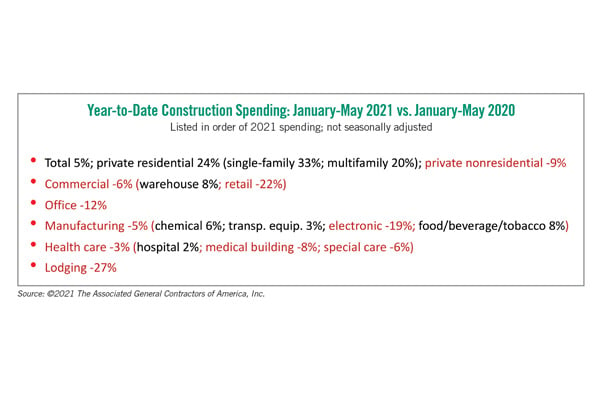

The Census Bureau reported on July 1 that total construction spending in the first five months of 2021 exceeded the year-to-date total in 2020 by 5%. However, that masked the huge disparity between private residential spending, which jumped 24% — including a 20% rise in multifamily construction — and the 9% drop in private nonresidential spending.

Among the nonresidential categories, only a few segments had turned positive, including warehouses, hospitals and some manufacturing niches. But forward-looking indexes from the American Institute of Architects and Dodge Data & Analytics suggest better times are just a few months away.

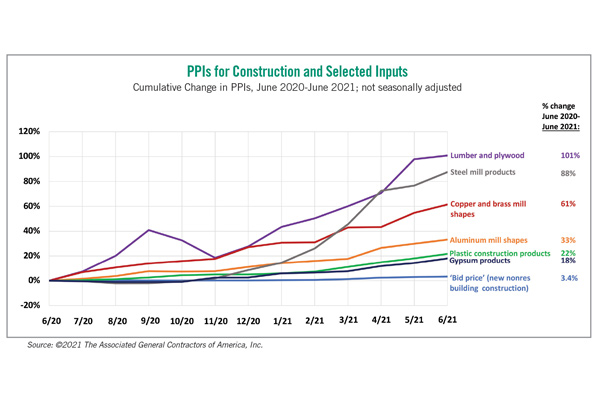

Contractors face two obstacles currently, with a third potential problem in the offing. First, materials costs have risen at unprecedented rates. The Bureau of Labor Statistics (BLS) estimated in mid-July that the producer price index (PPI) for inputs to construction industries — a measure of the cost of all materials and services used in every type of construction — soared 26.3% from June 2020 to June 2021. That was more than double the largest increase in any previous year.

Meanwhile, a measure of contractors’ bid prices, called the PPI for new nonresidential construction, climbed only 3.4% over the same period. The huge gap between contractors’ costs and bid prices meant many firms were passing on only a small fraction of the cost increases they were experiencing.

Numerous materials contributed to the meteoric rise in costs. The PPI for steel mill products jumped 88% over 12 months. The index for copper mill shapes leaped 61%. The PPI for aluminum mill shapes climbed 33%, while the index for plastic construction products increased 22% and the PPI for gypsum products went up 18%.

One item that had an even larger gain — lumber and wood products, which doubled in price over the year — has had a steep price decline since the PPI data were collected in mid-June. The price plunge has reportedly led some developers to restart multifamily projects they had shelved. But that decrease will hardly make a dent in the costs that most nonresidential contractors are absorbing.

The second major problem has been the unreliable supply chain. With lead times of as much as 11 months for bar joists and four to six months for roofing materials, some owners have been postponing projects. Even when goods are ready to ship from factories or ports, shortages of truck drivers and railcars complicate on-time completion of projects.

One more worry is the impact that the Delta variant might have on the construction workforce. Hospitalization rates have jumped among unvaccinated individuals. And many more individuals are incurring lingering symptoms that may keep them from returning to work or being fully productive. Unfortunately, a recent report listed construction and extraction employees as the occupation group with the lowest vaccination rate and highest hesitancy to get vaccinated. Thus, the construction industry, more than most, has the potential of losing experienced workers to renewed virus outbreaks.

In sum, construction appears poised to climb out of the depths, but the nonresidential side remains far below 2019 peaks. As the economic recovery expands, prospects for construction are brightening. But materials costs, supply-chain bottlenecks, and possible outbreaks of the coronavirus make the strength and timing of that revival uncertain.

Ken Simonson is the chief economist with the Associated General Contractors of America. He can be reached at ken.simonson@agc.org.

RELATED ARTICLES YOU MAY LIKE