CRE Financing Transitions from LIBOR

SOFR, the new U.S. dollar replacement rate, differs in crucial ways from its longstanding forerunner.

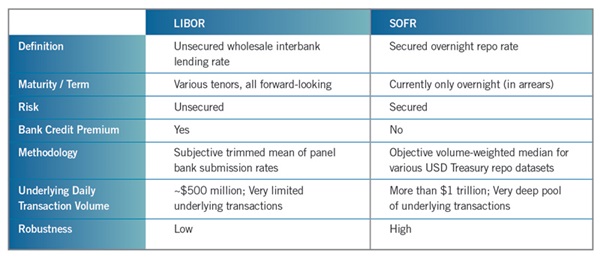

The London interbank offered rate, or LIBOR, is a critically important number in the world of finance. It is the basis for hundreds of trillions of dollars in contracts around the world. These include everything from complex derivatives to home mortgage loans.

According to calculations from the Federal Reserve, the estimated exposure for U.S. dollar LIBOR alone is approximately $200 trillion. Despite that large number, the underlying transactions that help determine LIBOR are a mere fraction of this amount. The rate is primarily based on submissions by certain banks based on what they estimate they would be charged to borrow from one another.

In 2012, as a result of various LIBOR scandals uncovered in the aftermath of the financial crisis, the U.K.’s newly created Financial Conduct Authority (FCA) was given regulatory oversight of LIBOR. Then, in 2014, the Financial Stability Board (FSB) published a report recommending the transition away from LIBOR to new reference rates supported by actual market transactions as opposed to bankers’ judgments. Soon after that, regulatory bodies and governmental agencies around the world worked to identify these new reference rates.

Finally, on July 27, 2017, FCA Chief Executive Andrew Bailey announced that the FCA would no longer compel banks to submit quotes for LIBOR after 2021. That left a little more than four years (now less than 18 months) for the eventual phasing out of LIBOR. The announcement galvanized global efforts to transition to these new reference rates.

The New Replacement Rate

In the U.S., the Federal Reserve formed the Alternative Reference Rates Committee (ARRC), a group of private-market participants, in November 2014 to identify a replacement rate for LIBOR. In June 2017, it announced the selection of the Secured Overnight Financing Rate (SOFR; pronounced “so-fer”) as its preferred rate.

SOFR is a broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury repurchase agreements (“repo”). Currently averaging well over $1 trillion in daily trading, transaction volumes underlying SOFR (which began publication on April 3, 2018) are far larger than the transactions in any other U.S. money market, and they dwarf the volumes underlying LIBOR.

Beyond transaction volumes, SOFR differs from LIBOR in other fundamental ways (as shown in the table below). For example, SOFR is an overnight, secured, nearly risk-free rate, while LIBOR is an unsecured rate with a “term structure,” as it is published at several different maturities (e.g., one-month, three-month, etc.).

Commercial Real Estate Finance and the LIBOR Transition

Commercial real estate (CRE) debt exposure to LIBOR is roughly $1.3 trillion, of which approximately $200 billion is securitized. The key securitized CRE/multifamily asset classes that reference LIBOR comprise both agency (i.e., Fannie Mae and Freddie Mac) and private-label commercial mortgage-backed securities (CMBS) and CRE Collateralized Loan Obligations (CRE CLOs). Within the CMBS market, single-borrower (SASB) CMBS transactions represent a significant component of LIBOR-based private-label transactions.

Over the past year, the CRE/multifamily finance industry has made meaningful strides in the transition from LIBOR to SOFR. Most new floating-rate CMBS transactions now include some form of the new contract language recommended by the ARRC. Among other things, this language identifies the waterfall of rates that would replace LIBOR following a transition event (or “trigger”) from LIBOR to SOFR.

In December 2019, Freddie Mac issued a CMBS transaction with a SOFR bond class; in February 2020, the Federal Housing Finance Agency (FHFA) announced that after December 31, 2020, Fannie Mae and Freddie Mac (the “GSEs”) would no longer purchase multifamily loans indexed to LIBOR.

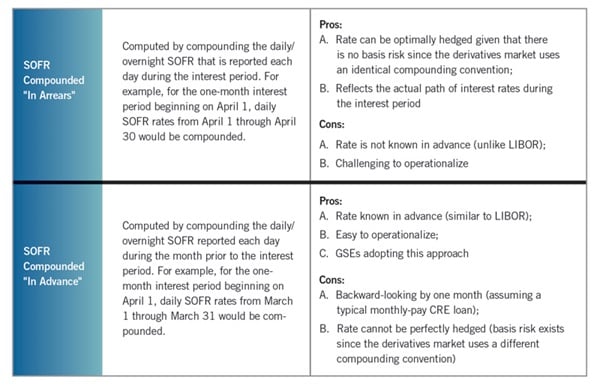

The market continues to await the issuance of private-label floating-rate CRE securitizations indexed to SOFR; the absence thus far is largely due to the current differences between LIBOR and SOFR as it relates to term. As noted earlier, SOFR is an overnight rate while LIBOR is published at several different maturities. A SOFR term rate is currently unavailable as the market waits for heightened volumes and liquidity in the SOFR derivatives markets. Until then, markets are utilizing an average of the daily SOFR rate in place of the relevant term LIBOR (e.g., one-month, three-month, etc.). However, this is easier said than done as a simple or compound average may be used. Further complicating the issue is that two conventions exist to determine the period of time over which the daily SOFR should be observed: “in arrears” or “in advance.” Each of these conventions has its advantages and disadvantages.

As a point of reference, the derivatives market has settled on using a compound average of SOFR “in arrears.” The securitizations market, however, has only coalesced around using a compound average, but has yet to decide on a convention (i.e., “in arrears” or “in advance”). The table above highlights the differences between these two conventions.

The pivotal difference in deciding between “in arrears” and “in advance” is that borrowers will want to know their interest rate before the beginning of the payment period and thus prefer “in advance,” while investors will want to know their return based on rates over the actual payment period, i.e., “in arrears.” According to research from the ARRC, differences in interest amounts calculated under the two conventions will tend to net out over the life of a loan if it remains outstanding for more than a few years. However, differences could crop up in any given period, and investors could gain or lose from one structure relative to the other. Frequency of payments could also be important, though the overall difference will typically be small in a loan that pays monthly compared to a loan with less frequent payment dates.

Next Steps for CRE Finance

The CRE Finance Council (CREFC) and the CRE/multifamily debt markets are narrowing in on a compounding convention for SOFR. Once this occurs, many other pieces in the transition will fall into place. These include the technology and systems enhancements needed to support SOFR across originations, trading and servicing. Many vendors have made significant progress, but are waiting on guidance from the industry on how it wants to use SOFR in transactions.

CREFC, which is a member of the ARRC, is working with its membership on selecting a compounding convention and a spread adjustment, as well other key sticking points, including facilitating vendor readiness, related to the LIBOR transition. Once the industry unites around these key conventions, it should pave the way for the issuance of SOFR-indexed CRE loans and securitizations, and accelerate the overall progression away from LIBOR.

Lisa Pendergast is executive director of the CRE Finance Council.