Will a radical change in the purpose of underutilized office buildings transform the market?

Housing affordability, especially in major metropolitan areas, has become a major social and political issue in the United States — one that has only been accentuated by the rapid rise in mortgage rates over the past 18 months. Although growth in home prices and residential rents has leveled off since a midpandemic run-up, there is nevertheless a systemic shortage of affordable housing to accommodate the generation of young adults who will be ready to form new households in the coming years. According to the National Multifamily Housing Council, the shortage of apartments alone will exceed 4 million by 2035.

Coinciding with this lack of housing is a structurally challenged commercial office market, the result of a pandemic-driven demand shock that has left some office buildings facing an existential crisis. Since the beginning of 2020, the office vacancy rate in the U.S. has risen from 9.5% to 13.3%, the highest ever observed by CoStar. Currently, nearly 20% of the space in ostensibly Class A rental buildings in the nation’s top 30 markets is vacant.

Facing the possibility of the large-scale functional obsolescence of office buildings, building owners, city leaders and a variety of real estate industry professionals have put forth the notion of converting underutilized offices into apartments. On its face, the idea has obvious merit. However, digging deeper into the details of past successful conversions shows that the rigid requirements that make such adaptive reuse financially feasible are likely to restrict the scope of future conversion activity to a few projects.

Defining the Criteria

Developers with experience in office-to-residential conversions emphasize three factors that stand out in making an office a viable candidate for conversion: location, floorplate size and cost. The last of these items has become more challenging in recent months, with the financing environment stifling much would-be development activity. Beyond this, there are also political considerations that can affect the feasibility of conversions.

As is always the case with real estate, everything starts with location. Industry practitioners report that, in some cases, conversion costs can be more costly than ground-up development. One implication of this is that, in the absence of robust public support, the premium rents that go with a desirable location are crucial for a financially successful conversion.

These prime locations bring competition from other developers, including retail and hospitality investors. This is one reason CoStar has tracked only about 20 major office-to-hotel conversions across major central business districts in the past five years.

Physical Profile

Apartments require a shorter distance from the center to the exterior walls than do offices. This is to accommodate access to windows and emergency egress, as well as to maximize the possibility of using existing elevators, staircases, plumbing, HVAC and other building systems.

This physical feasibility can be approximated by the size and shape of the building’s floorplate, or footprint. Historically, office buildings that have worked best for conversions are rectangular, with floorplates ranging from 8,000 to 12,000 square feet. Buildings with larger overall floorplates can still be good candidates, however, if their shape allows for a large amount of space near an exterior wall — think, for example, of buildings shaped like a capital “H,” “I” or “L.”

In practice, older buildings tend to work better for conversions, in part because they typically have smaller footprints. A CoStar examination of 34 completed office-to-multifamily conversions across the nation showed an average age of 93 years. Similarly, among the nearly 30 conversion projects currently underway, the average building age is 65 years.

Counting the Costs

Physical features are only part of the package for a conversion candidate. A building must also meet the financial conditions that will allow it to perform as a multifamily property. On the one hand, there must still be enough latent demand for housing in the area to make a multifamily property an attractive proposition. On the other hand, the building’s performance as an office should be poor enough that the prospective acquisition cost basis will allow for the necessary renovations to be performed while still having a cost-competitive multifamily property. This is not an easy balance to strike.

A recent ULI analysis of office-to-multifamily conversion projects shows that the typical hard costs of retrofitting a building range from $250,000 to $300,000 per unit. According to CoStar’s data, the current average market price of a multifamily property is just under $240,000 per unit. This implies that, on average, conversions would be difficult to execute financially even if the original asset were acquired for free. Of course, there are many locations where multifamily values are far higher than average, giving developers more breathing room.

Still, meeting the financial feasibility test will not be easy for most office buildings, even given the current softness of the office market. This is where public-sector incentives come into play. The reality is that some form of government subsidy is likely necessary to get potential office conversion projects out of the ground. (See “Governments Turning to Adaptive Reuse Legislation for Additional Housing”).

Sizing the Opportunity

These on-the-ground physical, financial and political realities mean that the actual number of suitable candidates for office-to-residential conversion is likely much lower than some optimistic projections suggest and that only a narrow set of existing office buildings are truly viable candidates for conversion to residential use.

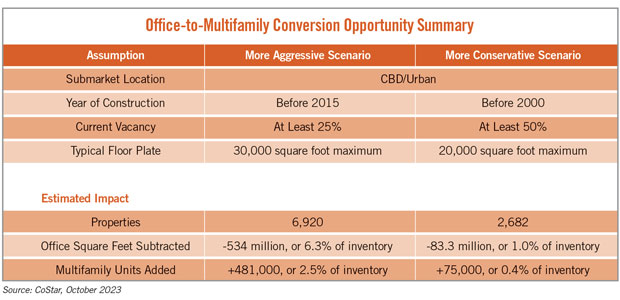

To quantify the possible scale of office-to-multifamily conversions, CoStar defined two scenarios, each representing a probable ceiling on what can be feasibly converted (see table below). For this analysis, physical feasibility is estimated using a building’s floorplate size. In the more aggressive scenario, buildings with footprints no larger than 30,000 square feet are considered; in the more conservative scenario, floorplate size is limited to 20,000 square feet or less.

To estimate acquisition cost-basis feasibility, current vacancy is used as a proxy. The more aggressive scenario uses 25% vacancy. This assumes generous public support to offset higher initial valuations and the additional cost of relocating in-place office tenants with term remaining on their leases. The more conservative scenario uses 50% vacancy.

Crucially, the analysis excludes office buildings in suburban areas based on the rationale that it will almost always be more attractive financially to develop new multifamily properties in the suburbs rather than conversions. It also excludes newer office buildings — those built prior to 2015 in the aggressive scenario and those built prior to 2000 in the conservative scenario — since those have performed comparatively better in the office market.

The Narrow Path

The results show that the ceiling on conversions is lower than some reports have suggested. Under the aggressive scenario, about 534 million square feet of office inventory in just under 7,000 buildings would come off the market. This is a meaningful amount but represents only 6.3% of current inventory. Furthermore, only about half of this amount is currently vacant. Assuming the office tenants currently occupying this space were relocated to other buildings, the overall impact on vacancy would be a decrease of about 260 basis points. This would bring the national vacancy rate nearer to its long-term historical average, but it would still be more than 100 basis points above where it was entering 2020.

On the multifamily side, the aggressive scenario would add about 481,000 units to the supply of apartments, or about 2.5% of the current inventory. This is about half the number of units currently under construction. It should also be noted that this estimate recognizes that conversions typically result in fewer units than new developments of comparable size because about 10% of the square footage is left unconverted (serving, for example, as first-floor retail). Of the remainder, the median unit size tends to be about 1,000 square feet.

In the more conservative conversion scenario, the impact on the overall office and residential markets is correspondingly smaller. It would remove about 2,700 buildings comprising 83 million square feet — 63 million of which are vacant — from the office stock. This would bring office vacancy down about 60 basis points and generate approximately 75,000 new apartment units, a mere 0.4% of inventory and less than 8% of the current construction pipeline.

The Impact

The office-to-multifamily conversion narrative holds intuitive appeal, particularly given the current state of the office market. Beyond the inherent logic, there are indications that key stakeholders, including public officials, are more willing than ever to ease the process of remaking underperforming buildings. As these efforts progress, there will doubtless be an increasing number of projects that are truly transformational to the neighborhoods in which they occur. Even so, the physical, economic and political realities of conversions all suggest that they are unlikely to have a significant impact on overall market fundamentals on either the office or the multifamily side.

Phil Mobley is the national director of office analytics at CoStar Group, and Jay Lybik is the national director of multifamily analytics at CoStar Group.

RELATED ARTICLES YOU MAY LIKE

Revitalization and Revenue: Office Conversions as a Way to Rebuild Cities

It’s not a panacea, but reuse can inject life into business districts.

Read More

Facility Managers Must Prepare for an All-Electric Future

Before that, many commercial buildings could benefit from hybrid electrification.

Read More

Developers Can Cash Out Tax Credits for Renewable Improvements

A major change to the tax code could greatly incentivize green construction in commercial real estate.

Read More