Data centers and power projects generate the most optimism in AGC’s annual business outlook survey.

Contractors are, by nature, optimists, believing they can tackle any project on time, on or under budget, and make a profit. But they appear less upbeat about their prospects for 2026 than they have in several years.

Every year, the Associated General Contractors of America conducts a construction hiring and business outlook survey, in partnership with Sage. The 2026 survey was open from Nov. 4 to Dec. 15, 2025, and drew 951 responses from contractors of all sizes in 49 states and Washington, D.C.

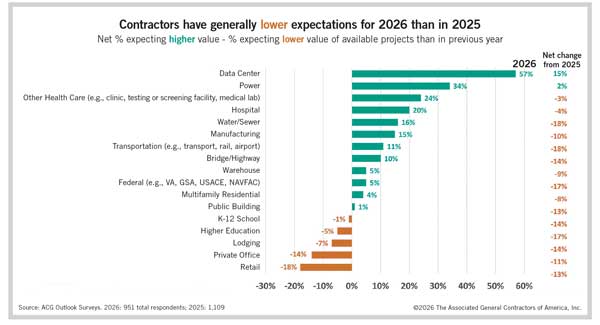

A key question was whether contractors expect the dollar value of projects available to bid on to be higher or lower in 2026 than in 2025. There were more optimists than pessimists for 12 of the 17 project types in the 2026 survey. But that was a decrease from 15 segments with net positive readings in the 2025 outlook survey. Furthermore, the level of optimism dropped — sharply, in most cases — for all but two categories.

The only exceptions were for data centers and power projects. The net reading for data centers — the percent of respondents who expect the market to expand minus the percent who expect it to shrink — jumped 15 points from a year ago to a net positive reading of 57 percentage points. Specifically, 65% of contractors expect growth, compared with just 8% who anticipate decline in data center construction opportunities in 2026.

The net reading for power projects, which range from renewable and conventional power generation to transmission lines, local distribution and storage, edged up 2 points to a net positive reading of 34.

Among segments of the greatest interest to developers and investors, the most optimistic outlook was for the catchall category of “other health care” — medical structures other than hospitals, such as clinics, testing and diagnostic labs, urgent care facilities and hospices. That niche drew a net positive reading of 24, which was down only slightly from the 2025 reading of 27.

Optimists outnumbered pessimists by 5 percentage points regarding warehouse construction and 4 percentage points regarding multifamily construction. However, these marks were less positive than the 2025 readings of 14 and 12, respectively.

Respondents were bearish on balance about lodging construction, with a net reading of -7, a sharp reversal from the 2025 reading of +7. And their pessimism deepened regarding two categories for which they already had negative expectations in 2025. The net readings slipped from -3 to -14 for private office construction and from -5 to -18 for retail construction.

One reason for the dyspeptic outlook is that owners have been holding back on projects. Among contractors who participated in the survey, 63% said at least one project in the past six months had been delayed, canceled or scaled back. The most common explanation, cited by 37% of participants, was “lack of funding or funding uncertainty (federal, state or private).” Nearly as many (34%) reported “financing unavailable or too expensive.”

Tariffs and other policy actions also played a role: 13% of firms cited “changes in demand/need due to tariffs,” and 22% pointed to “changes in demand/need due to other policy changes (federal funding, taxes, regulation, etc.)” as an explanation for project disruptions.

In short, contractors have a number of reasons for their subdued expectations for most project types in 2026. But there are many unknowns about how policies will evolve and whether those changes will spark an upturn in some types of construction.

Ken Simonson is the chief economist with the Associated General Contractors of America. Contact him at ken.simonson@agc.org.